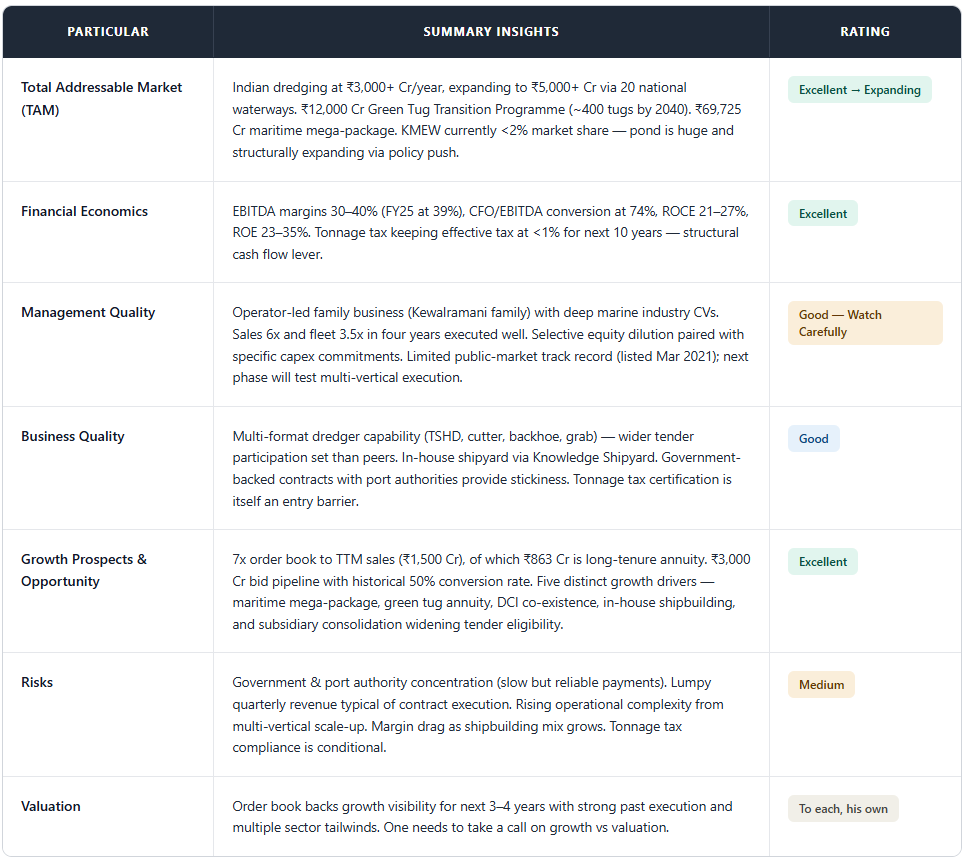

Knowledge Marine & Engineering Works: A Small Fish in an Expanding Pond

In our previous blog, India's Sea Awakening, we mapped contours of India's $70B maritime opportunity and teased 3 companies worth deeper look. This blog focuses on the most interesting one.

A few months ago, when we wrote our deep dive on the Indian shipping sector, one number kept coming back to us.

4%.

That’s the share of India’s own overseas trade that moves on Indian-owned ships. The rest 96% rides on Greek, Chinese, Japanese, and European vessels. Every spike in container rates, every bulk shipping squeeze, every LNG charter renegotiation, the bill lands on Indian shores. We estimated the cost of that dependency at $70-75 billion (₹5.8-6.2 lakh Cr) a year.

That earlier blog was the map of the ocean. This one is about a single island on it - small but sitting exactly where the current is starting to flow.

In case, you have not subscribed to our Newsletter, you may subscribe

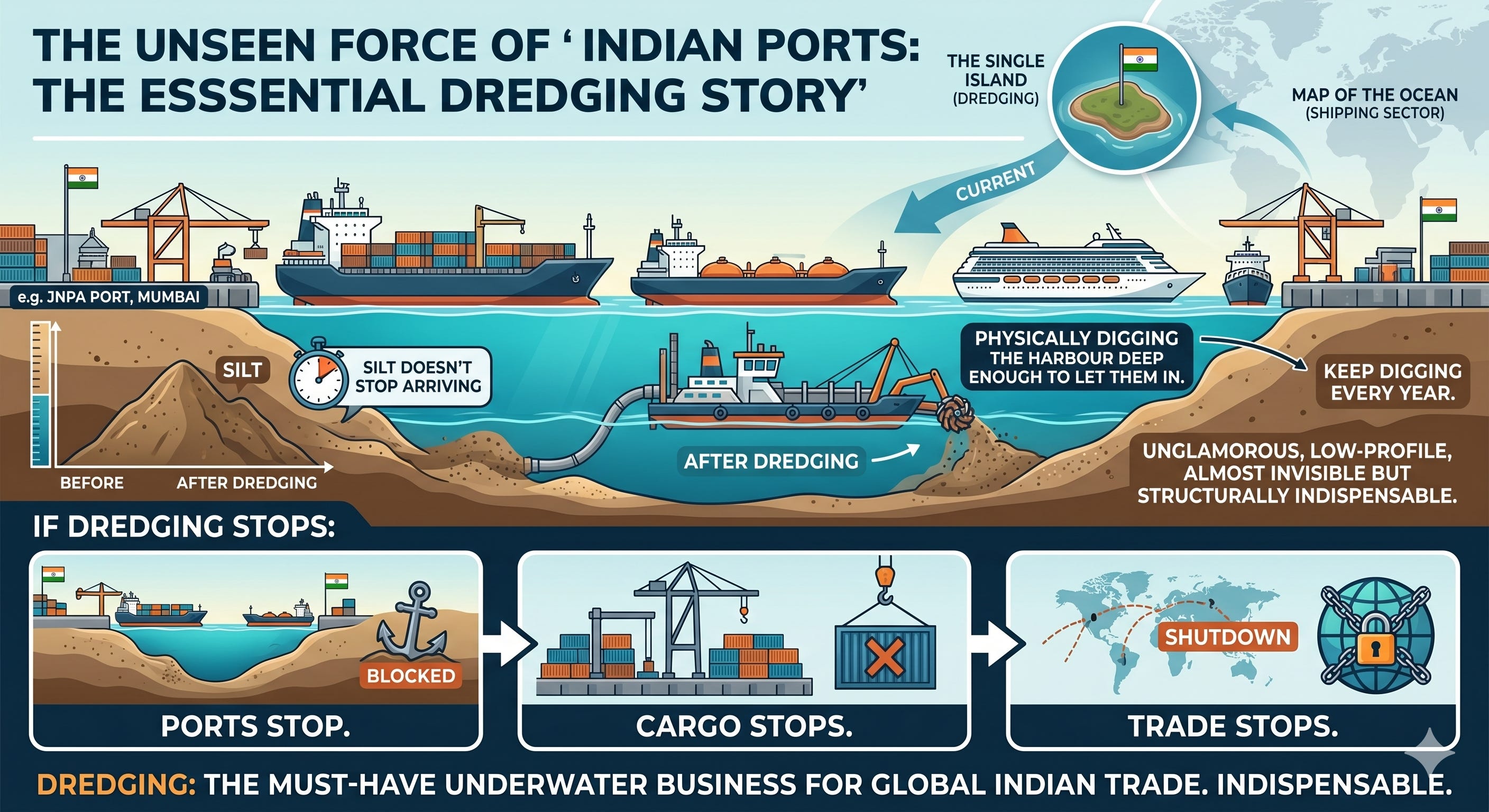

Here is the part of the shipping story that doesn’t make headlines:

Before a single container, tanker, or cruise ship can dock at an Indian port, somebody must dig the harbour deep enough to let it in. And keep digging, every year, silt doesn’t stop arriving just because the budget has been spent.

That somebody is a dredging company. Unglamorous, low-profile and structurally indispensable. The kind of business where, if it stops, ports stop. Cargo stops. Trade stops.

The company we are about to discuss is one of only two listed players in this space, and the one whose numbers kept catching our eye while writing the sector blog quietly compounding fleet from 13 to 45 vessels at 50%+ PAT growth.

Welcome to Knowledge Marine & Engineering Works Ltd (KMEW) - the invisible enabler of every coastal shipping rupee India hopes to earn back.

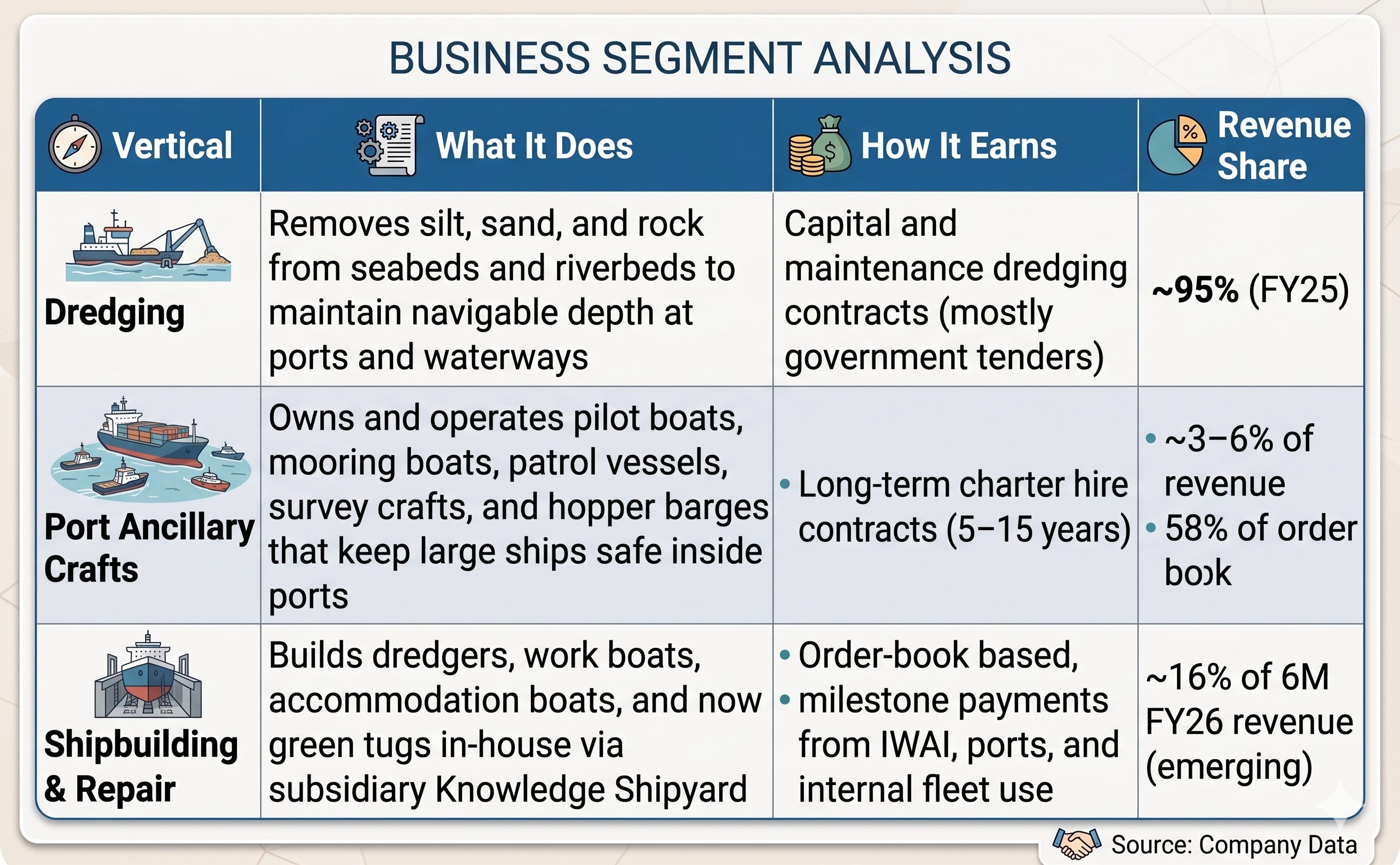

1. What Exactly Does KMEW Do?

Most maritime stories start with the ships. KMEW’s starts before the ships - at the harbour bed itself, doing the dredging. We investors keep looking for small fish in a big pond. However, there are managements who have the ability to keep expanding the pond (read total addressable market). We find Knowledge Marine’s management one of them.

Incorporated in 2015 and headquartered in Mumbai, KMEW is an ISO-certified marine company run by a team with collectively decades of experience in dredging, ship operations, and shipbuilding. Today, it operates across three core high-entry-barrier verticals in a span of 10 years, expanding the TAM from one segment to another:

Said simply, KMEW is in the business of making sure ports and waterways work. It does not own the ships that carry goods. It owns the equipment that ensures those ships have somewhere to go.

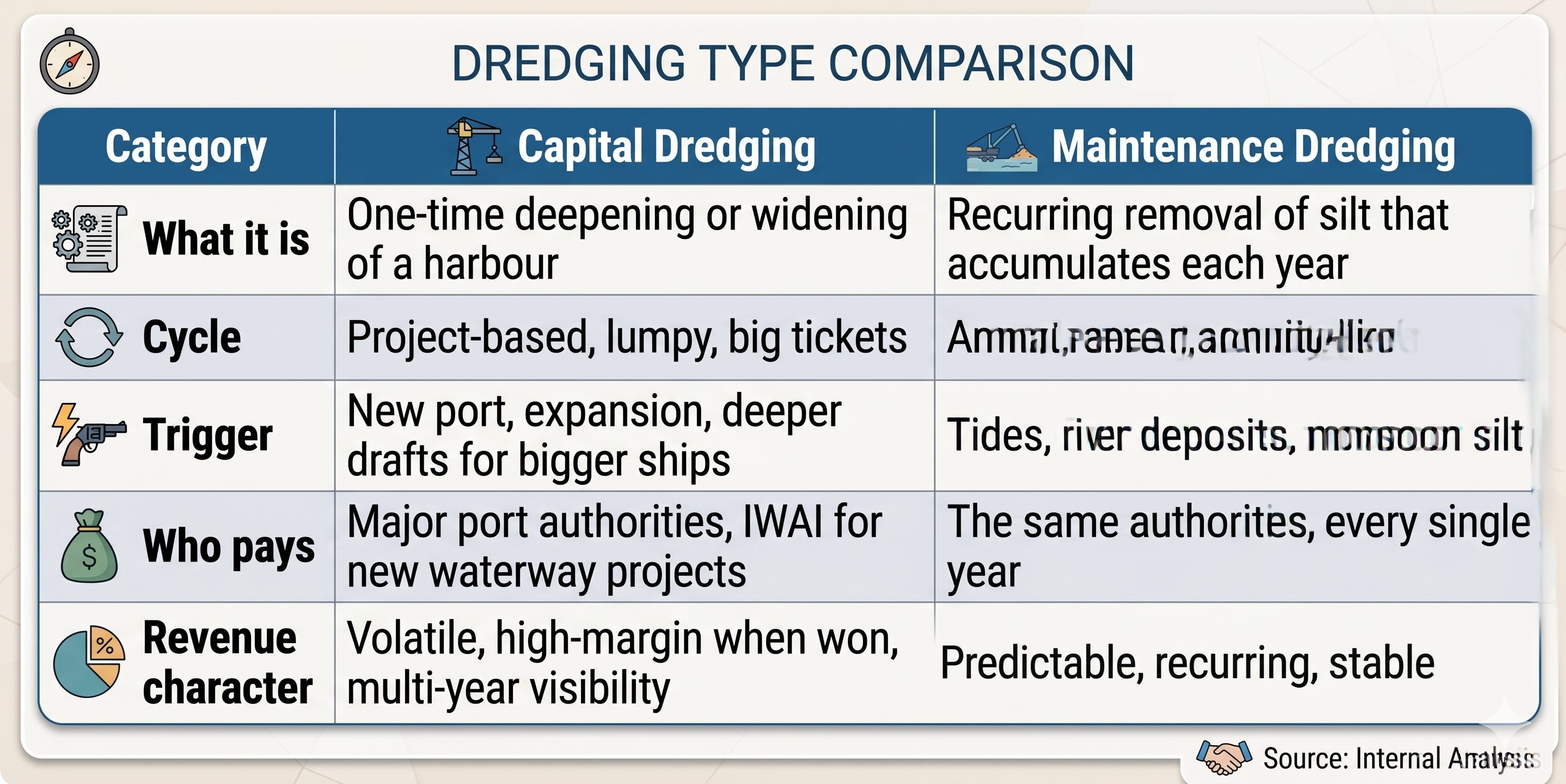

The Most Important Distinction in This Business: Capital vs Maintenance Dredging

If you only remember one thing about how a dredging company makes money, it should be this:

This split matters more than most people realise. Maintenance dredging is the closest thing to an annuity in the entire marine value chain - ports physically cannot stop maintaining their channels. The moment they do, vessels run aground and shipping traffic chokes. Skipping a year is not an option.

KMEW today is structurally over-indexed to maintenance dredging via long-term contracts with government port authorities. That recurring revenue base is what gives the business its margin stability and visibility - and it’s a distinction we’ll keep coming back to throughout the blog.

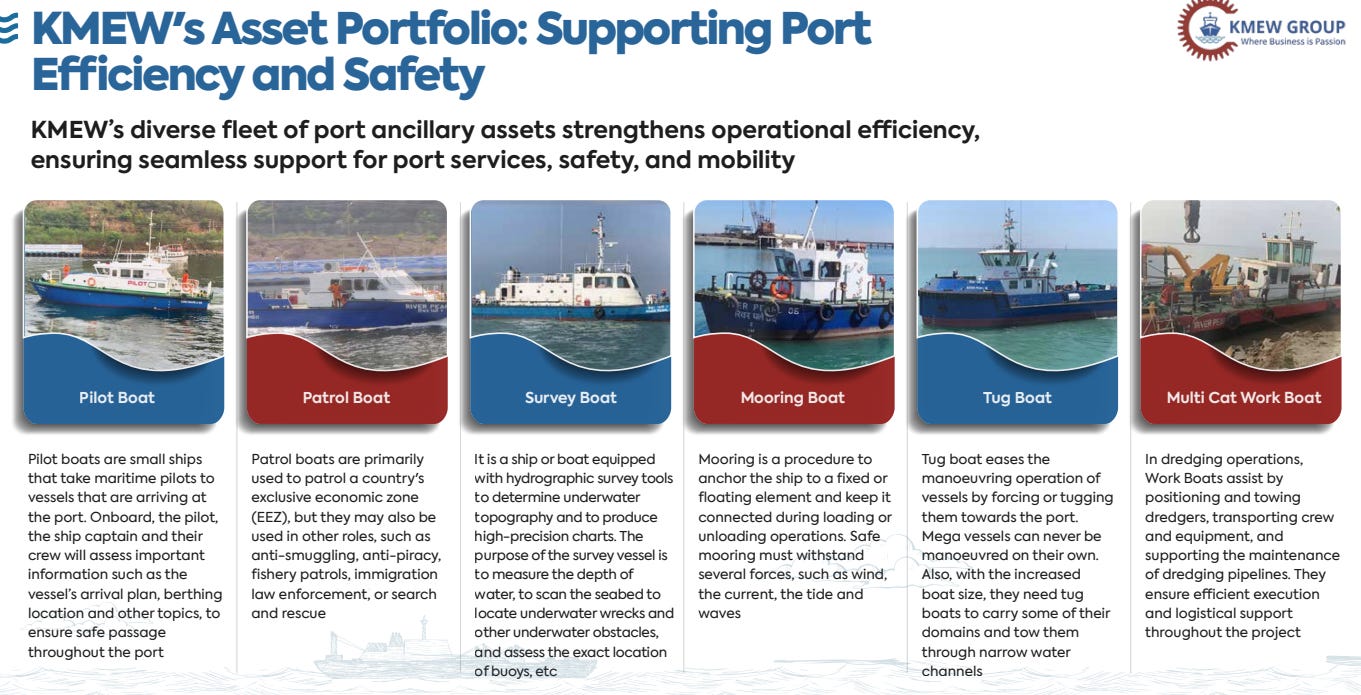

The company also operates across the full dredger format spectrum - TSHD (Trailing Suction Hopper), Cutter Suction, Backhoe, Grab Hopper - which means it can bid for almost any kind of dredging contract a port might float. Most peers specialise in one or two formats. This breadth itself is a moat.

Capital efficiency is the other piece. KMEW does not always buy expensive new dredgers - many of its assets are converted from used vessels and barges, modified in-house. The result: lower upfront capex and faster asset turns than a pure newbuild player would manage.

Who Actually Pays KMEW?

Almost entirely government bodies. The customer mix looks like this:

Major Port Authorities - Deendayal Port Trust (Kandla), VOC Tuticorin, Visakhapatnam Port, Paradip Port, Mumbai Port, New Mangalore Port

Inland Waterways Authority of India (IWAI) - for river dredging and inland waterway crafts

Dredging Corporation of India (DCI) - KMEW subcontracts smaller-format jobs from DCI for shallow-draft work that DCI itself does not service.

This customer profile shapes the whole business model. The good part: near-zero credit risk - government port authorities do not go bankrupt. The less good part: long sales cycles and slow payments. Debtor days at ~100 are not unusual, tender-to-award timelines can stretch 6–12 months, and government budget cycles can shift project start dates. The working capital and concentration risk we will discuss later flow directly out of this customer mix.

Geographically, KMEW is no longer a purely Indian operator. It took its first international assignment in FY21 (a dredging contract at Sittwe Port, Myanmar, followed by an overseas branch in Yangon) and entered Bahrain in FY24 with a sand-mining contract. Together, these geographies contributed around 40% of FY25 revenue - though Bahrain reflects project-specific lumpiness rather than a steady annuity stream. The international footprint matters more right now for the capability signal it sends to global tender committees than for steady-state earnings.

The business is clear. The customers are visible. But a small player can only ride a tailwind as far as the tailwind is willing to take it. The next question, then, is how big the pond KMEW is swimming in - and how fast is that pond growing.

2. The Opportunity: How Big Is the Pond, and How Fast Is It Growing?

We will not re-walk the entire Indian maritime story here - Sea Awakening has already done that work. Treat this section as a zoom-in: the specific pools of demand that flow through a company like KMEW, and how the recently announced ₹69,725 Cr maritime mega-package converts each of them from policy headlines into actual revenue lines.

The Sectoral Tailwind, in One Paragraph

The ₹69,725 Cr package is structured around four pillars - a Maritime Development Fund for capital availability, SBFAS 2.0 for shipbuilding subsidies, the Green Tug Transition Programme for port decarbonisation, and capacity augmentation of National Waterways.

The targeted outcome: India moving from <1% global commercial shipbuilding share to 5% by 2030, with domestic shipyard capacity scaling to 4.5 million GT by 2036. For dredging-led businesses that sit upstream of every port and waterway expansion, this translates into a near-decade-long demand pipeline. The full architecture is in the prior blog; what matters here is what the package adds up to for KMEW specifically.

The Four Sub-Pools KMEW Sits In

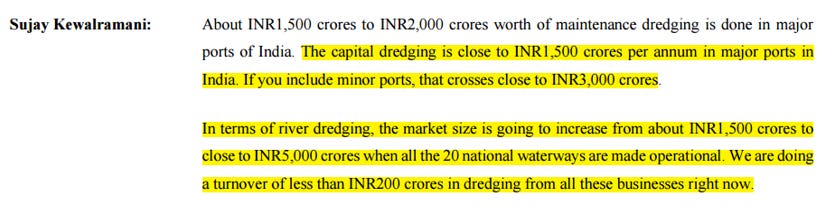

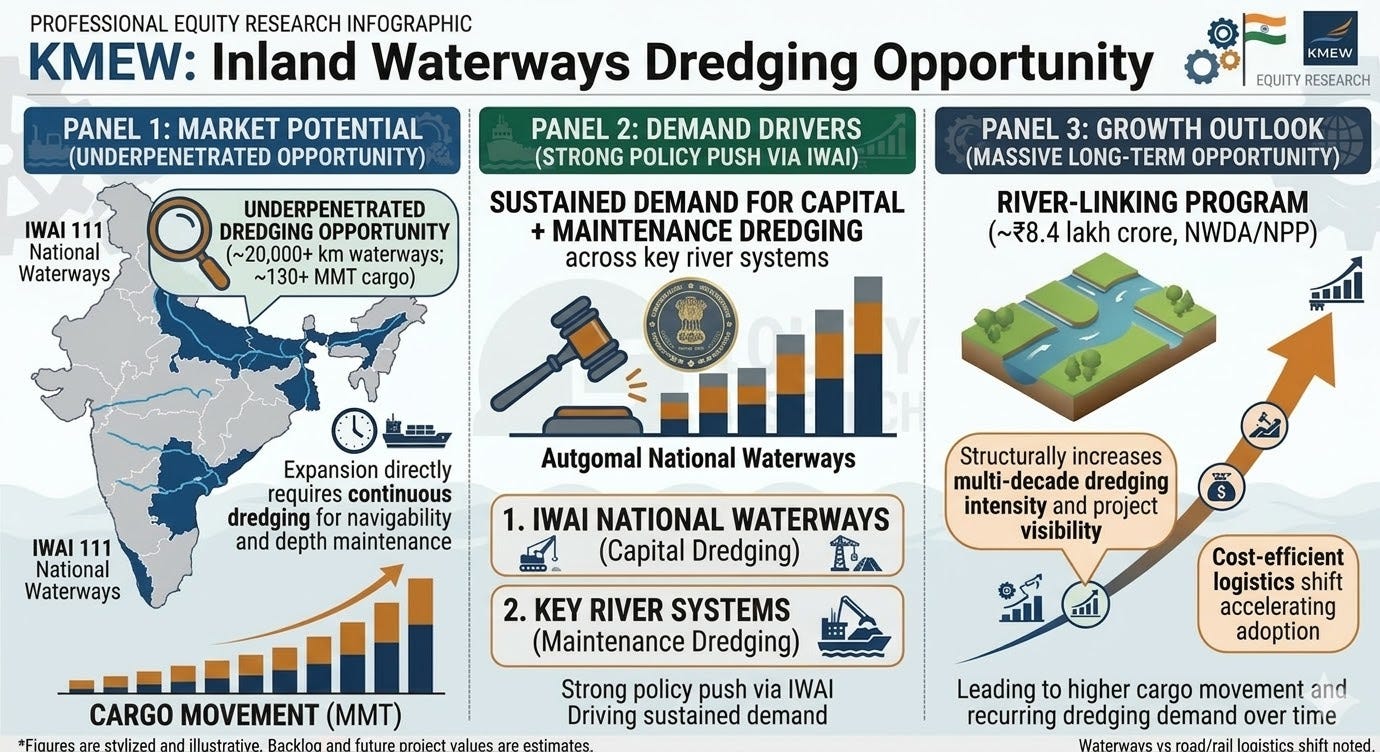

1. Port Dredging - ₹3,000+ Cr / year. India’s major ports execute roughly ₹1,500–2,000 Cr of maintenance dredging and ~₹1,500 Cr of capital dredging annually. Add minor ports and the addressable pool crosses ₹3,000 Cr. Maintenance is non-discretionary - ports physically cannot stop. This is the core of KMEW’s business today.

2. Inland Waterways Dredging - ₹1,500 Cr scaling to ₹5,000 Cr. Inland River dredging today is a ~₹1,500 Cr market. As all 20 National Waterways become fully operational, the same pool grows to ₹5,000 Cr+.

Sitting behind this is the long-tail NWDA river-linking program - ~₹8.4 lakh Cr aggregate program cost (per PIB), of which dredging is only a fraction. Only Ken-Betwa (₹44,605 Cr) is in active execution today; every additional link that materialises adds multi-decade incremental dredging demand.

3. Green Tug Transition Programme - ₹12,000 Cr Government Investment. GOI has mandated 100% green tug adoption across all 12 major ports by 2040, replacing ~400 conventional diesel tugs with electric / clean-fuel equivalents. Lifecycle fleet revenue: ₹36,000 Cr cumulative, with peak annual deployment of ₹2,000–3,000 Cr / year through 2027–2034. Policy-mandated capex, not market-driven demand - which means it cannot soften with cycles.

4. Indigenous Shipbuilding under SBFAS 2.0. IWAI and major ports are now mandated to procure dredgers and ancillary vessels from domestic yards. KMEW’s Knowledge Shipyard is one of a small handful of yards qualified to bid. Genuine reverse-import-substitution demand - vessels that would have come from Korean or Chinese yards now flowing into the domestic supply chain.

The Combined View

So, What Is KMEW’s “Real” Addressable Market?

When you stack port dredging, inland waterway dredging, the green tug build-out, and the small-vessel shipbuilding pool together, the directly addressable opportunity for a company like KMEW is comfortably north of ₹6,000–8,000 Cr per year over the next 5–7 years, with the green tug fleet adding long-tenure annuity revenue on top.

KMEW today does roughly ₹235 Cr in revenue. That is less than 2% market share in a pond that itself is growing.

Please note that this stock has been part of our SME and Microcap advisory services where we look for below Rs 4000 Cr market cap companies who have potential to make it big, typically a ‘small fish, big pond’ setup.

You may explore our SME and Microcap Advisory services in this link:

Qualitative SME & Microcap Investment Advisory service

Weekend Special Discount: We are running a limited-time flash sale for our readers this weekend. Use coupon code SISMENEW05 to get a 5% discount on our SME & Microcap services. Note: This offer is strictly valid for this weekend only and expires this Sunday at midnight.

A growing pond is one thing. Whether the small fish swimming in it has the build to keep growing alongside is another. KMEW has changed shape four times in roughly ten years and that trajectory is worth walking through before we get to the financials.

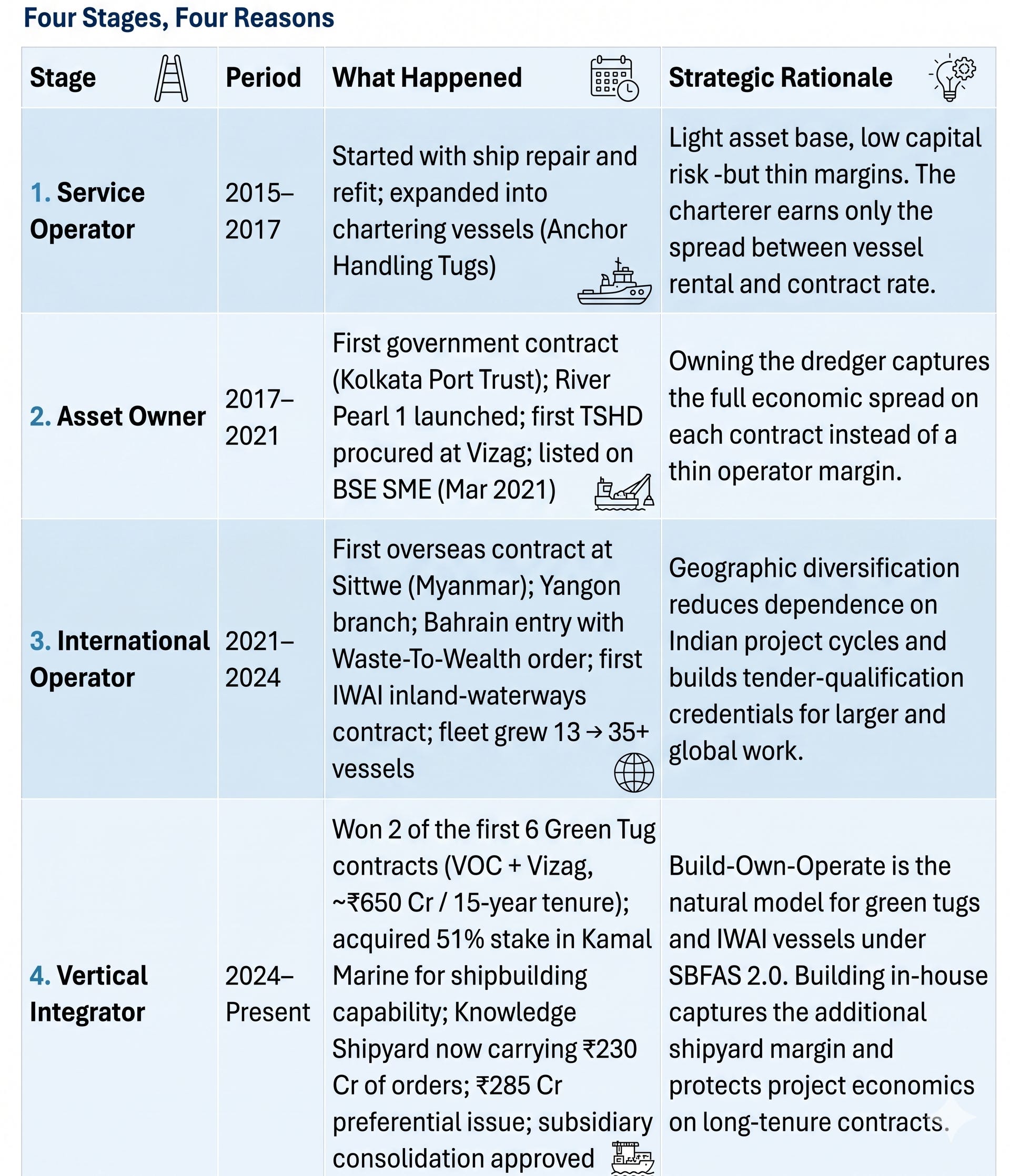

3. Evolution: From Chartering Boats to Building Them

KMEW has been a different company at each stage of its existence. It started in 2015 as a ship-repair and chartering outfit. By 2021 it was a listed asset owner running its own dredgers. By 2022 it was bidding overseas. Today it builds vessels in its own yard. Four distinct business shapes in roughly ten years - and each shift moved the company further up the margin pool.

The pattern is consistent: each stage didn’t just add a capability; it internalised a margin that was previously paid out to someone else. From operator’s spread → asset owner’s spread → builder’s spread. That’s a slow, deliberate climb.

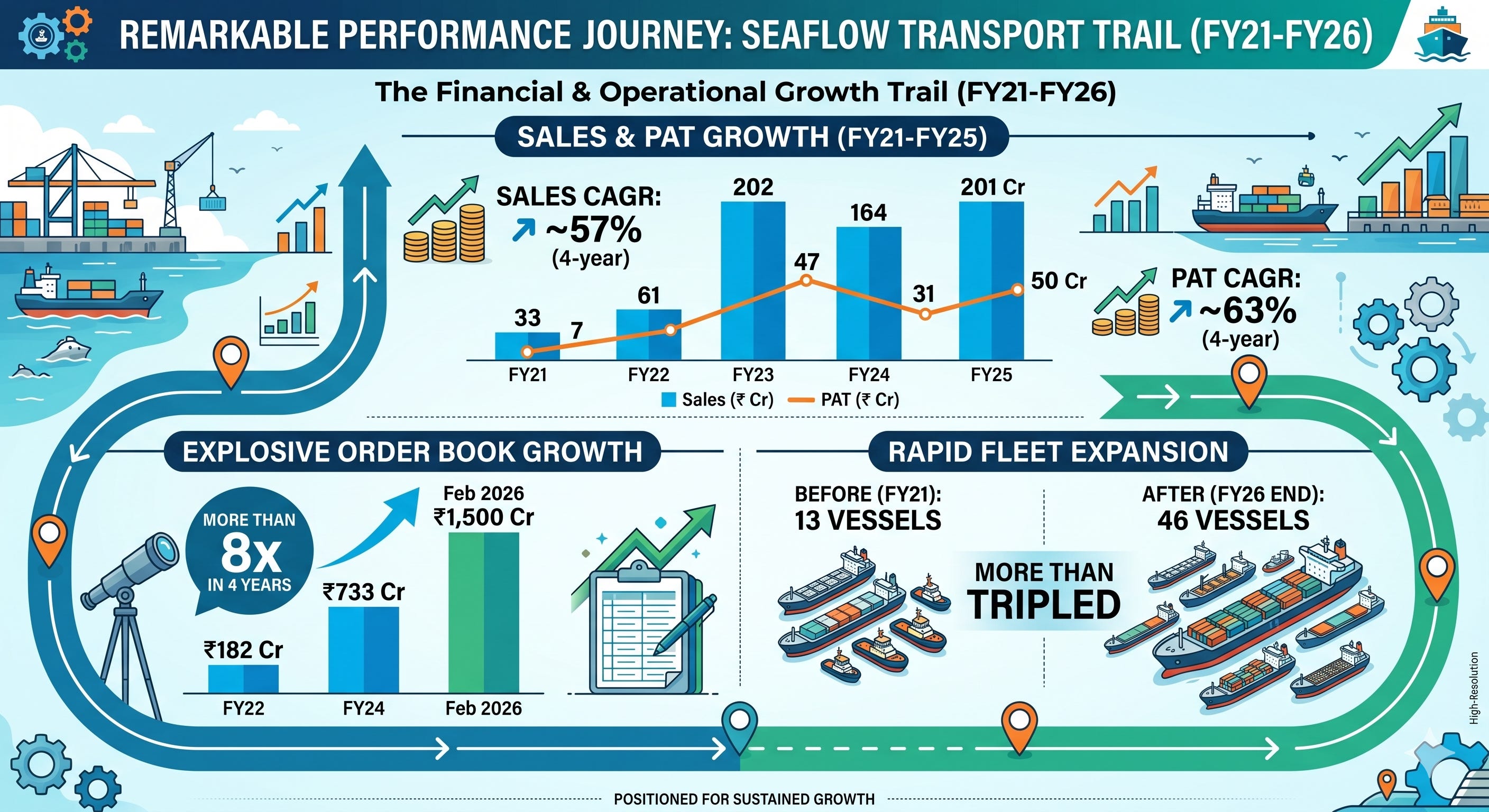

The Financial Trail

A quick note before the numbers section: the FY24 line will look like a setback at first glance. It isn’t - it’s the flip side of an FY23 spike when several large contracts hit peak execution at once. We unpack it properly in Section 4.

Sales 6x, fleet 3.5x, order book 8x in four years. The next section is where this gets stress-tested - what margins, cash flows, and working capital did while the company was changing shape underneath them.

4. Financial Analysis: What the Numbers Really Say

This is a high-growth, high-asset, high-margin business - but every line item tells a slightly different story. Revenue is up 6x in four years, though year-on-year reads jagged. Margins are healthy but normalising. Order book is 7x sales, but tenure skewed. Cash flow is healthy operationally but thin at the FCF level.

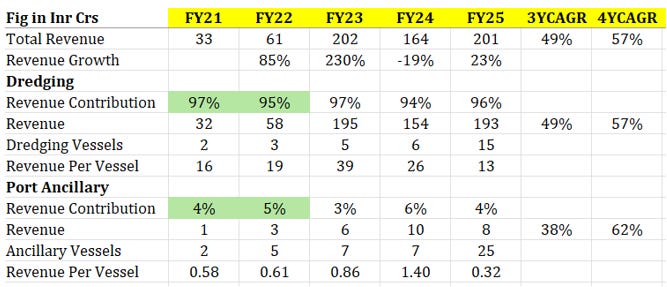

4.1 Revenue: Six Times in Four Years, and the Mix is Shifting

KMEW’s topline has grown roughly 6x in four years - ₹33 Cr (FY21) → ₹201 Cr (FY25), a 4-year CAGR of ~57%.

The FY24 number throws people off. A 19% revenue drop looks like a setback - until we see what came before it. FY23 was the spike. Several large dredging contracts hit peak execution simultaneously in FY23, lifting revenue 230% in a single year. FY25 recovered to near-FY23 levels; 9M FY26 is already at ₹188.66 Cr

The more interesting story is the mix. Until FY24, dredging contributed 95-97% of revenue every single year. The H1 FY26 split is genuinely different - Dredging & Ancillary at 66%, Shipbuilding & Repairing at 22% (negligible 18 months ago), Bahrain 8%, Myanmar 4%. The shipbuilding inflection was triggered by the Kamal Marine acquisition (51% stake at ~₹1.22 Cr), which gave KMEW the in-house capability to execute IWAI orders flowing through Knowledge Shipyard.

Topline compounding remains strong; the bigger shift is that “pure-play dredging company” no longer describes KMEW.

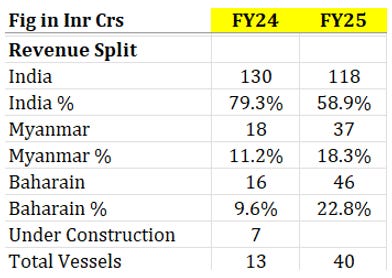

4.2 Geographic Mix: A One-Year Bend, not a New Curve

FY25 looked like the year KMEW became a meaningfully overseas business - India’s share moderated from ~79% to ~59%, with Bahrain at ~23% and Myanmar at ~18%. The caveat: the Bahrain spike was a single sand mining contract -non-recurring.

FY25’s geographic split highlights overseas execution capability, but treat it as project-driven, not steady-state.

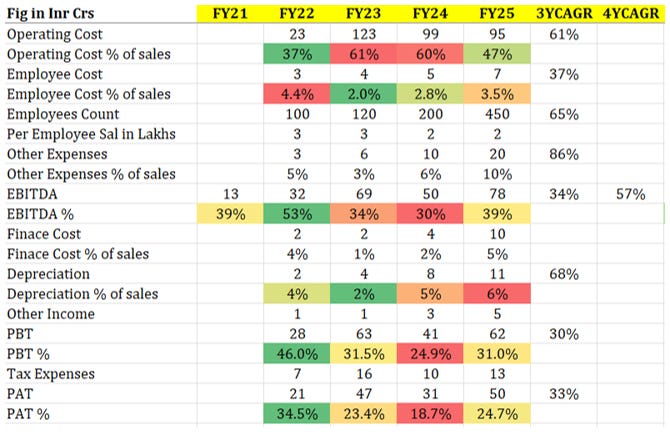

4.3 Margins & Cost Structure: Normalised but Structurally Strong

EBITDA margins have moved through a wide band - 39% → 53% → 34% → 30% → 39% across FY21-FY25. The volatility is contract-mix and one-off-driven, not operational instability. The current sustainable range is 30-40%.

Cost structure under the margin tells the operating-leverage story: operating costs as % of sales improved from 61% (FY23) → 47% (FY25), employee costs stayed at 3-4% even as headcount went 100 → 450. Asset-led model in action.

The shipbuilding mix shift will compress blended margins mildly going forward - shipbuilding economics structurally run lower (12-18%) than dredging (35-40%). As shipbuilding scales, expect blended EBITDA to settle in the 30-35% range as a realistic medium-term anchor.

Margins have stabilised at structurally healthy levels; mild compression ahead as shipbuilding scales, but still excellent for a contract execution business.

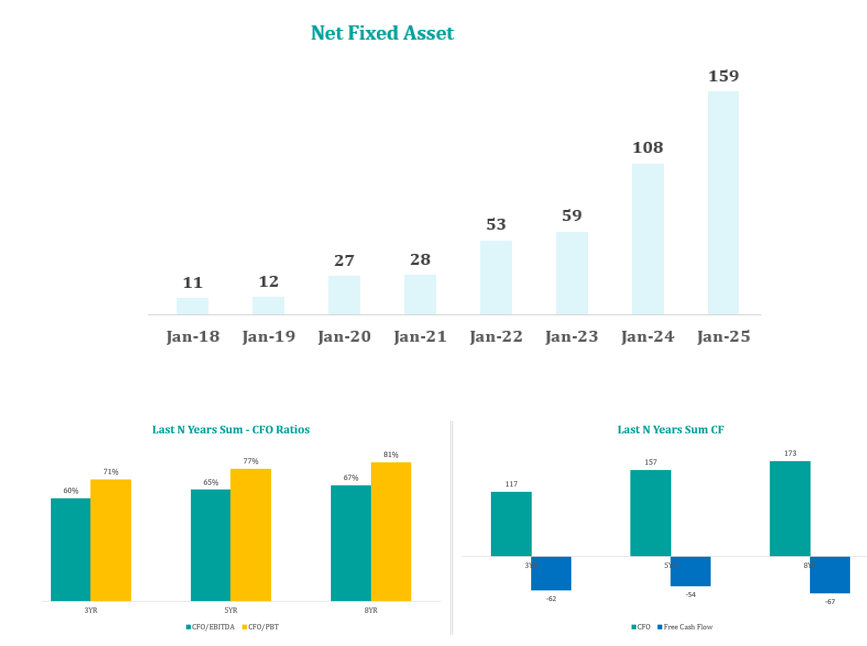

4.4 Cash Flow & Asset Turns: The Build-Out Signature

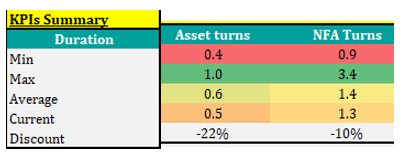

CFO/EBITDA conversion sits at a healthy 74% in FY25. Asset base has grown 5x in four years - ₹28 Cr → ₹159 Cr in net fixed assets. This is heavy reinvestment: capex has consistently been >100% of CFO, leaving FCF negative or marginally positive. Not a flaw - a feature of building ahead of revenue ramp.

NFAT has normalised to 1.3x in FY25 from a peak of 3.4x in FY23. The FY23 spike was the Bahrain contract (high revenue, low local asset base) -strip that out and underlying NFAT was always 1.3-1.5x. Current levels reflect the sustainable asset-turn profile.

To fund the next leg of capex, KMEW raised ₹285 Cr through a preferential issue - ₹183 Cr to fleet capex, ₹30 Cr to working capital, ₹71 Cr to general corporate / shipbuilding.

Build-out phase signature: cash generation healthy, free cash thin, asset base building ahead of utilisation.

4.5 The Tonnage Tax Lever - A 10-Year Cash Flow Reset

KMEW has transitioned from corporate tax (~25% on profits) to the Tonnage Tax regime, which calculates tax based on registered tonnage rather than reported profit. Effective tax rate drops to <1% of turnover, locked in for 10 years.

What this changes: post-tax cash flow rises sharply, and bidding competitiveness improves - a bidder with <1% effective tax can price 5-7% lower on 15-year contracts and still earn the same return as a corporate-tax peer.

The benefit is conditional on seafarer training compliance and tonnage thresholds - any lapse triggers a rollback to 25% tax. Worth tracking annually, but the immediate-term risk is low.

Numbers tell us what held together through the journey. The next question is who held it together and whether the same hands are equipped for a phase that’s about to get materially more complex.

5. The People Running the Show

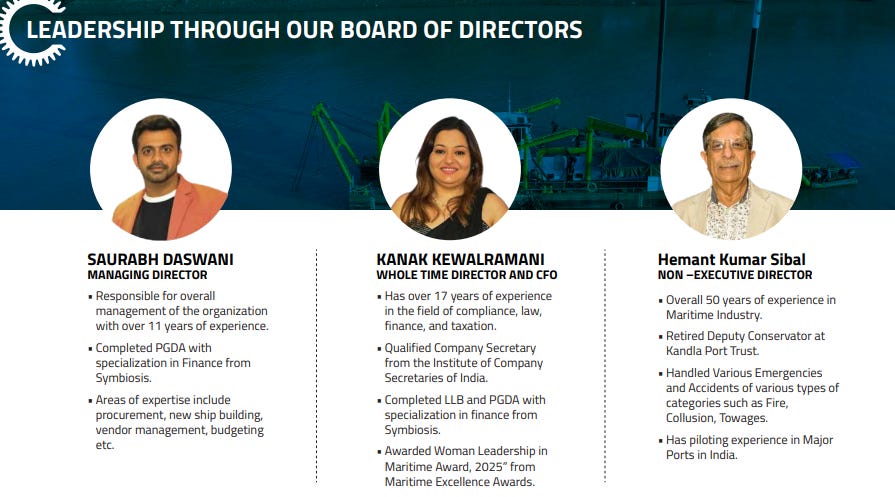

KMEW is an operator-led family business. The senior management is concentrated in the Kewalramani family, with careers built inside the marine industry.

The structure

The board has three members: Saurabh Daswani (MD, 11 years’ experience, finance background), Kanak Kewalramani (Whole Time Director & CFO, 17 years in compliance and finance), and Hemant Kumar Sibal as Non-Executive Director. Sibal’s profile is genuinely useful - 50 years in maritime, retired Deputy Conservator at Kandla Port Trust. For a company that bids heavily on port authority contracts, having a former port authority insider on the board carries weight beyond the average NED appointment.

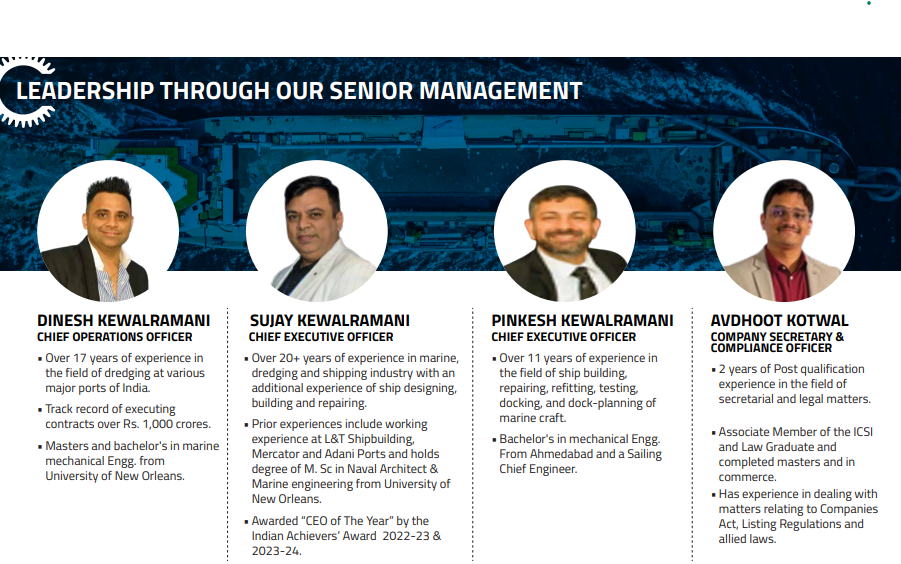

The Senior Management layer:

Sujay Kewalramani (CEO) - 20+ years across L&T Shipbuilding, Mercator, and Adani Ports; M.Sc Naval Architecture & Marine Engineering from University of New Orleans. The deepest operating CV in the team.

Dinesh Kewalramani (COO) - 17 years executing dredging contracts at major Indian ports; the company’s deck cites a track record of executing contracts over ₹1,000 Cr.

Pinkesh Kewalramani (CEO, Shipbuilding) - 11 years in shipbuilding, repair, refitting, and dock-planning; Sailing Chief Engineer.

Three observations:

The team has built credentials before they built the company. This is not a case of promoters who suddenly discovered marine engineering. They have significant experience in this field.

Hands-on operators not hired professionals. The COO has previously executed dredging contracts. The CEO has run shipbuilding floors. This level of operational immersion shows up in execution quality, particularly when the company scaled from 13 vessels to 46 in 4 years without major project delays.

Capital allocation discipline so far has been good. The recent Kamal Marine acquisition (51% stake for ₹1.22 Cr against an FY23 peak turnover of ₹20 Cr) was small, strategic, and immediately accretive in terms of shipbuilding capability.

A capable team is necessary but not sufficient. The harder question is whether the opportunity in front of them is large and specific enough to convert four more years of execution into the next phase of compounding.

6. Where the Next Leg of Growth Comes From - and Whether KMEW is Built to Catch It

Section 2 made the case for why the pond is large and growing. This section answers the harder question: when the policy package lands, when the green tug contracts get tendered, when the inland waterway dredging budgets release - does this small company have what it needs to convert demand into revenue?

The honest answer is that KMEW hasn’t been sitting still waiting for the policy push. Five things, specifically, are worth highlighting.

1. Capability Built Ahead of Demand: The Four-Format Fleet

KMEW has gone from 13 vessels at IPO to 46 by FY26-end - including ~26 dredgers across all four major formats (TSHD, cutter suction, backhoe, grab hopper). Most peers specialise in one or two formats. In an L1-tendered industry, the bidder who can credibly claim execution capability across formats has a structurally wider participation set than a single-format peer.

Combine that with 100% vessel utilisation (no idle capacity) and the operating posture is straightforward: capacity already built; currently fully deployed, additional fleet now being added against contracted demand - not speculative additions hoping for orders.

2. Build Capability Brought In-House: The Kamal Marine Move

Through FY21-FY24, KMEW operated other people’s vessels. Through FY24-FY26, it has shifted to building them in-house via Knowledge Shipyard.

The move that quietly enabled this was small in ticket size but full cycle in implication. KMEW acquired 51% of Kamal Marine & Engineering Works for ~₹1.22 Cr (implied 100% valuation ~₹2.4 Cr) - roughly a tenth of one year’s revenue for an entry into shipbuilding, repair, and refitting.

Why it matters: every tug KMEW builds in-house is a tug where they capture the shipyard margin on top of the operator margin across the 15-year contract. A pure operator earns one spread. KMEW now earns two spreads on the same vessel. The shipbuilding order book is currently ~₹230 Cr (₹185 Cr from IWAI), and management has guided that Knowledge Shipyard could touch ₹500-700 Cr of standalone topline within three years.

3. Proof Points on the Highest-Value Tailwind: Green Tugs

The Green Tug Transition Programme is the single largest demand pool highlighted in Section 2. KMEW’s positioning here isn’t aspirational - it’s already on the scoreboard.

Of the first six green tug contracts awarded under GTTP, KMEW has won two - VOC Port (Tuticorin) and Visakhapatnam, totalling ₹650 Cr in lifetime revenue across 15-year tenures. A 33%-win rate against larger and more entrenched players including Samson Maritime and Polestar.

The economics here are different from a typical project. Build-Own-Operate contracts mean KMEW builds, owns, deploys, and earns daily charter for 15 years. Revenue is annuity-like, not project-lumpy. Lenders treat 15-year visibility favourably, which means future expansion can lean on debt rather than equity dilution.

The pipeline behind this: roughly 30 more green tug contracts expected over the next 5-7 years across the 12 major ports. If KMEW maintains anywhere near its current win rate, this single segment could anchor ₹2,000-3,000 Cr of cumulative lifetime revenue - for a company doing ₹201 Cr today, that’s a meaningful number.

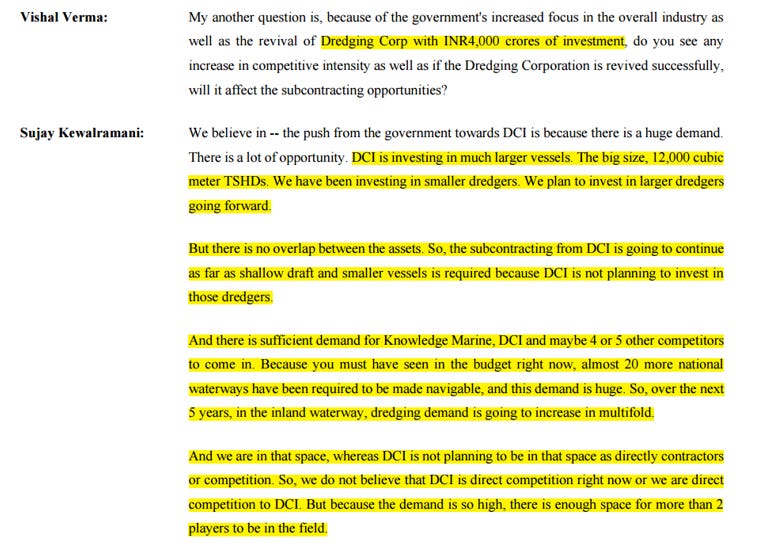

4. The DCI Question: Why the Big Player Helps, Not Hurts

When investors first hear about DCI’s ₹4,000 Cr fleet modernisation, the instinctive reaction is “big incumbent + capex push = small player gets crowded out.” The data says the opposite.

DCI is investing in large 12,000 cubic-meter TSHDs for major port capital dredging. KMEW operates smaller dredgers for shallow-draft work, river dredging, and inland waterways. Different vessel sizes, different project sizes, different bid pools. DCI’s expansion expands the overall pie by raising port capacity, which drives more maintenance dredging at minor ports and inland waterways -KMEW’s home turf. KMEW also subcontracts for DCI on shallow-draft jobs DCI cannot service.

So, the read for investors: the rising tide lifts both, just at different vessel sizes.

5. Tender Eligibility Quietly Widened: The Internal Consolidation

A small-sounding move with materially bigger practical implications: a scheme of amalgamation approved in Jan 2026 merges two of KMEW’s existing subsidiaries -Indian Ports Dredging Pvt Ltd (IPDPL) and Knowledge Infra Port Pvt Ltd (KIPPL) - into the parent.

Why this matters: in tender-driven industries, “prior work experience” is a hard qualifying criterion. Larger contracts often require the bidding entity to have directly executed a minimum project size. By consolidating subsidiary credentials into the parent, KMEW becomes eligible to bid for tenders that the standalone parent would have failed to qualify for.

Small administrative move on paper. Materially wider tender participation set in practice.

A capable team is necessary but not sufficient. The harder question is whether the opportunity in front of them - the policy push, the tailwinds, the contracts in pipeline - is large and specific enough to convert the next four years of execution into the next phase of compounding.

7. Risks That Could Bend the Story

Every shipping investment thesis has a shadow side. KMEW’s fault lines:

Risk 1: Concentration on Government / Port Authority Customers

The vast majority of KMEW’s revenue comes from port authorities (DCI, Deendayal Port, Kandla, Tuticorin, Vizag, IWAI) and government-owned entities. This means:

Tender delays are real. A 6–9-month delay in award decisions can push revenue recognition into the next financial year.

Payment cycles are slow. Debtor days at ~100 reflect this. Healthy WC management is critical.

Policy reversals or budget cuts can disrupt the pipeline. Less likely given the visible mega-package, but possible.

Risk 2: Lumpy, Non-Linear Revenue

This is structural for the business model, not a flaw. But it does mean:

Quarter-to-quarter results will be volatile. A single dredger going for maintenance or a single contract closing 30 days later can move the quarterly number by 5-10%.

Risk 3: Execution Complexity Rising Sharply

Going from a single-vertical dredging company (FY21) to a multi-vertical business covering dredging, port crafts, green tugs, and shipbuilding (FY26) is a massive jump in operational complexity:

Shipbuilding has notoriously high cost-overrun risk if execution discipline slips.

Building 24+ vessels in-house at Knowledge Shipyard while also scaling dredging operations is a real test.

The team’s track record so far is strong, but the difficulty curve is steep from here.

Risk 4: New Business Margin Drag

As shipbuilding scales, blended margins will compress. Management is confident overall margins can hold via mix offsets, but if green tug buildouts face delays or shipbuilding margins disappoint, the headline EBITDA% could disappoint, and the stock currently prices in margin maintenance.

Risk 5: Tonnage Tax Compliance

The <1% effective tax benefit is conditional on:

Maintaining certain minimum on-board seafarer training requirements

Filing compliance certificates with the IT department

Reinvesting tax savings into vessels (per the scheme’s intent)

Any lapse could trigger a rollback to the corporate tax rate (~25%), which would materially impact post-tax economics. Worth monitoring annually.

Risk 6: L1 Competitive Intensity

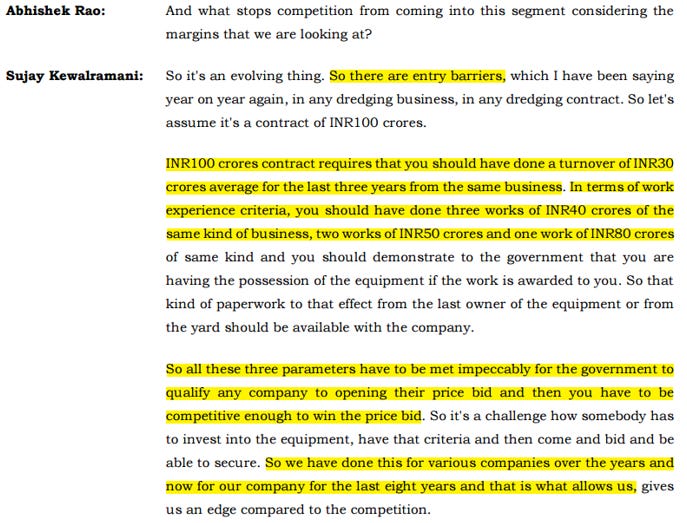

Government tenders are largely L1 (lowest bidder). As more players enter the dredging and tug space, attracted by the same tailwinds we’ve described, margin compression on new contracts is plausible. KMEW’s defence is its multi-format capability, execution track record, and now in-house build economics on tugs. But this is not a moat that lasts forever.

A good business at the wrong price is still a bad investment. The next section weighs what KMEW is asking the market to pay against the growth and risks just laid out.

8. Valuation: What’s on the Table

Companies which are growing at a high rate, even though trade at higher multiples, may continue to do so, till high growth phase is on. This itself may provide returns similar to EPS growth. However, once the growth falters, market may derate the stock which may lead to wealth destruction. Hence, valuation is “to each his own” depending on one’s portfolio construct, holding period expectation, exit plan and risk appetite.

Closing Thoughts

KMEW sits at the intersection of multiple maritime sub-themes - dredging, green tugs, inland waterways, indigenous shipbuilding - inside a single small-cap entity. The preparations of the last five years (fleet built ahead of demand, shipyard brought in-house, early green tug wins, ₹1,500 Cr order book) read like a business that was getting ready for a phase that hasn’t fully arrived yet.

Closing Thoughts summarizing the business.

For Investors Who Like:

Small-cap exposure to a sector tailwind that is still in early innings.

Small fish in a pond which is expanding as management is executing its multi vertical expansion.

Decent entry barriers for given company size

Asset-backed contract revenue

Long runway for growth with quiet compounding on P&L including sales and profitability.

At Scientific Investing, in our investment advisory services, we love identifying unique businesses, interesting business models and like to purchase at the right price, thus, benefitting our customers, by making appropriate recommendations and building portfolios, custom to customer risk appetite.

Ready to Find the Next Quiet Compounder?

If you appreciate this level of deep-dive, practitioner-grade research on under-followed small caps and micro caps, let us do the heavy lifting for you.

Get instant access to our top high-growth stock recommendations, model portfolios, and real-time updates through the Qualitative SME & Microcap Investment Advisory Service.

🚨 Exclusive Weekend Special Discount: Use coupon code SISMENEW05 at checkout to unlock an extra 5% discount on your subscription. This coupon code is valid only for this weekend and expires this Sunday at midnight.

[Explore Our SME & Microcap Service Now]

Explore our Ultrasmall cap, Multicap and Quants offering here:

Explore our custom investment advisory services here:

Join our custom advisory waitlist:

We tried to figure this out few months back in our “Shipping” sector Supersession for PRACTITIONER subscribers.

At Scientific Investing, in our education services, we keep teaching our many such unique case studies through our sector, business, market sessions backed by multiple tools and resources, driven by data.

Join our PRACTITIONER+SIMBA subscription for more such sessions and to learn about your path to financial freedom:

https://practitioner.scientificinvesting.in/

Thanks for reading Scientific Investing Newsletter! This post is public so feel free to share it.

DISCLAIMER: Please note these documents are intended to initiate academic curiosity and help understand any business at a 1st level, encouraging the right questions. This information should not be considered as a buy or sell recommendation. We publish multiple such academic documents/contents, and anything published by Scientific Investing should be considered only for educational purposes and not a buy or sell recommendation. Kumar Saurabh, founder, Scientific Investing, is also a Partner at Jaima Scientific Ventures LLP. Jaima Scientific Ventures LLP is registered with SEBI under SEBI (Investment Advisors) regulations, 2013 with registration number INA000021030.

This content here is meant purely for educational purposes and not meant for any investment or trading purposes and kindly do not consider it as advice or recommendation. The companies discussed may or may not be part of our portfolio, and we may buy or sell any holdings without prior notice.

Please note that the stock in discussion is part of our and client’s portfolio and should not be considered as BUY or SELL recommendation

| A guest post by

|

👍👍👍👍👍👍👍

❣️❣️❣️❣️❣️❣️❣️

🙏🙏🙏🙏🙏🙏🙏